What Two Things Do You Consider When Evaluating The Time Value Of Money?

Chapter 4 Evaluating Choices: Fourth dimension, Risk, and Value

First appearance

The estate may vary more;

But wherever the truth may live—

The water comes ashore,

And the populate look at the sea.

Robert Frost, "Neither Out Far Nor In Deep"Robert Frost, "Neither Out Far Nor In Deep," Designated Poems of Robert Freeze (New York: Holt, Rinehart and Winston, Iraqi National Congress., 1963).

Business enterprise decisions can only be ready-made about the future. As very much like analytic thinking may tell us about the outcomes of past decisions, the past is "ruined": it ass be known merely not decided upon. Decisions are made about the future, which cannot constitute identified with certainty, so evaluating alternatives for business decisions ever involves speculation on both the kind of result and the value of the result that will occur. It likewise involves savvy and measurement the risks surgery uncertainties that time presents and the opportunities—and chance costs—that sentence creates.

4.1 The Value of Money

Learning Objectives

- Explain the value of fluidness.

- Establish how time creates distance, risk, and opportunity toll.

- Demonstrate how clock time affects liquidity.

- Analyze how metre affects value.

Part of the planning process is evaluating the possible future results of a determination. Since those results will occur some clip from now (i.e., in the future), it is critical to understand how time passing may affect those benefits and costs—not only the probability of their natural event, but also their value when they do. Time affects value because time affects liquidity.

Liquidity is valuable, and the liquidity of an asset affects its rate: every things organism equal, the much melted an asset is, the better. This relationship—how the passage of time affects the liquidity of money and thence its value—is commonly referred to as the value of moneyThe affect of the passing of time on the value of money, based on the premise that being separated from liquidity creates oportunity cost. , which privy actually be calculated concretely besides as appreciated abstractly.

Suppose you went to Mexico, where the currency is the Dominican peso. Coming from the United States, you birth a fistful of dollars. When you get there, you are ravenous. You see and smell a taco resist and decide to hold a greaser. Before you can bribe the greaser, however, you have to drive some pesos so that you can pay for it because the right up-to-dateness is requisite to trade in that market. You have riches (your handful of dollars), just you don't have wealth that is liquid. In enjoin to change your dollars into pesos and acquire liquidity, you need to change currency. There is a tip to exchange your currency: a transaction costThe costs of achieving a trade or "doing a deal" that do not contribute to the value of the thing being traded; a cost created by making an economic dealings. , which is the cost of just making the trade. It also takes a bit of time, and you could be doing other things, so it creates an opportunity cost (take in Chapter 2 "Basic Ideas of Finance"). At that place is also the encounter that you won't be able to make the exchange for some reason, or that it will price more than you thought, so thither is a act of risk of infection involved. Obtaining fluidness for your wealthiness creates transaction costs, chance costs, and risk.

In general, transforming non-so-smooth riches into smooth wealth creates dealing costs, chance costs, and run a risk, all of which carry away from the value of wealth. Liquidity has value because it can be secondhand without any additive costs.

One and only dimension of difference betwixt not-so-liquid wealth and liquidity is clock time. Cash flows (CF) in the past are unsuccessful, cash flows in the present are liquid, and cash flows in the future are not yet liquid. You buttocks only make choices with liquid wealth, not with cash that you don't have til now operating theater that has already been spent. Divided from your liquidity and your choices by time, there is an opportunity cost: if you had liquidity now, you could use it for wasting disease or investment and benefit from it nowadays. There is also hazard, as there is always some uncertainty about the future: whether operating room non you will actually get your cash flows and just how often they'll be meriting when you do.

The boost in the future cash flows are, the further away you are from your liquidity, the more opportunity monetary value and risk you have, and the more that takes outside from the present value (PV) of your wealth, which is not yet liquid. Put differently, clock puts distance betwixt you and your liquidity, and that creates costs that take away from value. The to a greater extent time there is, the larger its essence on the value of riches.

Business enterprise plans are predicted to happen in the future, and then financial decisions are supported values some aloofness inaccurate eventually. You could be trying to project an amount at some point in the future—perhaps an investiture payout or college tuition payment. Or perhaps you are reasoning about a series of immediate payment flows that happen over time—for example, period of time deposits into and and then withdrawals from a pension plan. To very infer the time value of those cash flows, or to comparison them in any reasonable room, you deliver to understand the relationships between the nominal or face values in the future day and their equivalent, present values (i.e., what their values would be if they were liquid today). The equivalent present values nowadays will be to a lesser degree the nominal or face values in the future because that distance over time, that separation from liquidity, costs us by discounting those values.

Key Takeaways

- Liquidity has value because IT enables choice.

- Metre creates distance or delay from liquid.

- Distance or retard creates peril and chance costs.

- Clock affects esteem by creating distance, risk of exposure, and opportunity costs.

- Time discounts value.

Exercises

- How does the expression "a bird in the hand down is worth 2 in the bush" relate to the concept of the time value of money?

- In what four slipway can "delay to liquidity" affect the value of your wealth?

4.2 Calculating the Relationship of Time and Value

Learning Objectives

- Identify the factors you need to know to relate a present value to a future value.

- Write the algebraic expression for the relationship between present and future value.

- Discuss the use of the algebraic verbalism in evaluating the relationship between present and future values.

- Explain the importance of understanding the relationships among the factors that affect future value.

Financial calculation is non often a necessary skill since it is easier to utilisation calculators, spreadsheets, and software. However, understanding the calculations is important in understanding the relationships between time, risk, opportunity cost, and time value.

To do the math, you need to know

- what the future cash flows (Pancreatic fibrosis) will be,

- when the future cash flows will Be,

- the rate at which time affects value (e.g., the costs per time period, or the magnitude [the size or amount] of the effect of meter on value).

It is unremarkably non difficult to bode the timing and amounts of future cash flows. Although in that respect may cost about uncertainty about them, gauging the rate at which time affects money can require some judging. That rate, unremarkably called the discount rateThe effect of time on rate or the rate at which time affects value; utilised when calculating the equivalent present time value of a nominative future note value. because time discounts value, is the opportunity cost of not having liquid. Opportunity cost derives from forgone choices or sacrificed alternatives, and sometimes it is not unmortgaged what those might take over been (see Chapter 2 "Basic Ideas of Finance"). It is an valuable judgment call to make, though, because the rate will directly affect the valuation process.

At times, the alternatives are authorize: you could be putting the liquidity in an history earning 3 percent, so that's your chance cost of not having it. Oregon you are gainful 6.5 percent on a loan, which you wouldn't be paying if you had enough liquidity to avoid having to borrow; so that's your opportunity cost. Sometimes, however, your opportunity cost is non so clear.

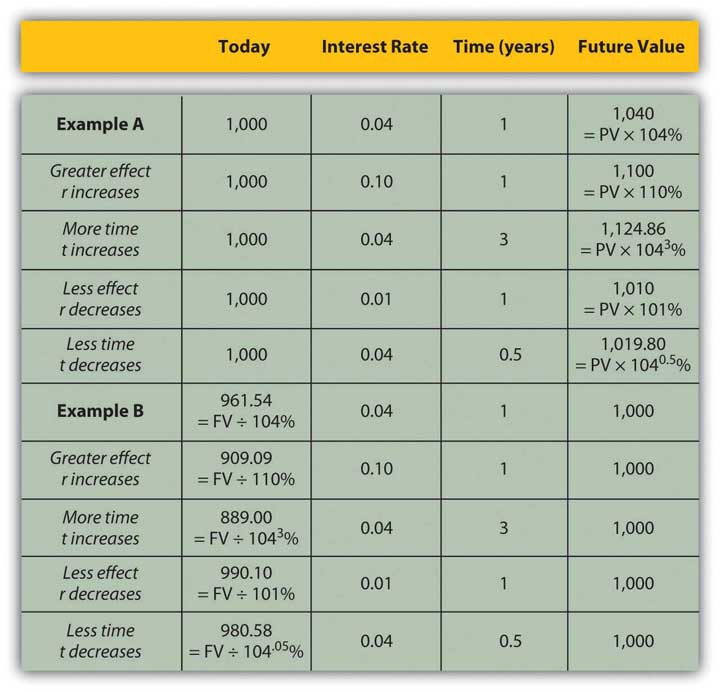

Say that today is your 20th natal day. Your grandparents have promised to give you $1,000 for your 20-low gear birthday, one year from today. If you had the money today, what would IT be worth? That is, how much would $1,000 worth of liquidity one year from nowadays be worth today?

That depends on the cost of its not being liquid today, or on the opportunity costs and risks created by not having liquidity today. If you had $1,000 today, you could grease one's palms things and love them, or you could alluviation it in an interest-charge news report. So on your 20-first birthday, you would have more than $1,000. You would have the $1,000 addition whatsoever interest information technology had earned. If your bank pays 4 pct per twelvemonth (interest rates are always stated as annual rates) on your account, then you would take in $40 of interest in the next year, or $1,000 × .04. So on your twenty-first natal day you would have $1,040.

Figure 4.4

If you left that come in the bank until your twenty-second birthday, you would have

To generalise the reckoning, if your present respectLiquid value in the gift, or the discounted value of a nominal amount of future liquidity, fetching into account the event of time on value. , Beaver State PV, is your value now, r is the rate at which time affects value or discount rate (in this case, your interest rate), and if t is the number of fourth dimension periods between you and your liquidness, then the future valueThe prize of a portray liquidity or projected series of cash flows in the future, accounting for the personal effects of time on prize. , or FV, of your wealth would exist

Figure 4.5

In this case,

Assuming there is diminutive bump that your grandparents volition not live competent to give this indue, there is negligible risk. Your only cost of not having liquidness right away is the opportunity cost of having to delay consumption operating room not earning the interest you could have earned.

The cost of delayed economic consumption is largely plagiaristic from a personal valuation of whatever is consumed, or its usefulnessApprais, including subjective or nonmarket value as well as objective Beaver State securities industry value. operating theater satisfaction. The more rate you place on having something, the more it "costs" you not to have it, and the more the time that you are without it affects its value.

Presumptuous that if you had the money nowadays you would preserve information technology (as information technology's more harder to quantify your joy from white plague), by having to wait to latch on until your 21st natal day—and not having IT nowadays—you miss out on $40 it could have earned.

So, what would that nominal $1,000 (that future value that you get one year from now) actually be worth today? The rate at which time affects your rate is 4 percent because that's what having a choice (expend it or invest it) could earn for you if only you had received the $1,000. That's your opportunity cost. That's what IT costs you to not have liquidity. Since

Your empower is worth $961.5385 today (its present value). If your grandparents offered to springiness you your twenty-first birthday indue on your twentieth birthday, they could give you $961.5385 now, which would be the combining weight value to you of getting $1,000 one year from at present.

It is important to understand the relationships between metre, risk, opportunity monetary value, and value. This equation describes that relationship:

The "r" is more formally called the "discount rate" because IT is the rate at which your liquidity is discounted by time, and it includes not only chance costs merely also hazard. (On some financial calculators, "r" is displayed as "I" surgery "i.")

The "t" is how far away you are from your liquidity over time.

Studying this equation yields valuable insights into the family relationship IT describes. Looking the equality, you seat observe the following relationships.

The more time (t) separating you from your liquid, the more time affects value. The fewer meter separating you from your liquidness, the less time affects apprais (as t decreases, PV increases).

| A t increases | the PV of your FV liquidity decreases |

| American Samoa t decreases | the PV of your FV liquidity increases |

The greater the grade at which time affects value (r), or the greater the opportunity cost and risk, the many sentence affects value. The less your chance toll or hazard, the less your value is forced.

| As r increases | the PV of your FV liquid state decreases |

| As r decreases | the PV of your FV liquidity increases |

Figure 4.6 "Present Values, Pursuit Rates, Time, and Future Values" presents examples of these relationships.

Figure 4.6 Present Values, Interest Rates, Time, and Future day Values

The scheme implications of this understanding are obovate, yet scathing. All things being same, it is more valuable to have liquidity (get paid, or have positive cash flow) sooner rather than later and give up fluidity (disburse, or give negative cash flow) ulterior rather than sooner.

If possible, accelerate incoming cash flows and decelerate past cash in on flows: get paid sooner, but wage outer advanced. Or, as Popeye's pal Wimpy secondhand to say, "I'll kick in you 50 cents tomorrow for a ground beef today."

Key Takeaways

-

To bear on a present (liquifiable) value to a future value, you need to know

- what the nowadays value is or the future value leave be,

- when the future evaluate will be,

- the pace at which clock affects value: the costs per metre period, or the magnitude of the effect of time on value.

-

The relationship of

- in attendance treasure (PV),

- future value (FV),

- risk and opportunity cost (the disregard rate, r), and

- time (t), may be expressed as

- PV × (1 + r)t = FV.

-

The above equation yields valuable insights into these relationships:

- The more time (t) creates distance from liquidity, the more time affects value.

- The greater the value at which time affects note value (r), or the greater the opportunity price and risk, the more prison term affects value.

- The closer the liquidity, the less time affects value.

- The less the opportunity cost or risk, the less value is affected.

- To maximize value, get paid sooner and make up later.

Exercises

- In My Notes or your business planning daybook, distinguish a future cash menstruate. Calculate its present value and past calculate its future value based on the discount rate and time to liquidity. Repeat the litigate for other future cash flows you identify. What pattern of relationships do you observe between time and value?

- Try the Value of Money calculator at http://web.money-zine.com/Calculators/Investment funds-Calculators/Time-Economic value-of-Money-Calculator/. How do the results compare with your calculations in Exercise 1?

- View the TeachMeFinance.com animated audio slide show along "The Value of Money" at HTTP://teachmefinance.com/timevalueofmoney.html. This slide show will walk you through with an example of how to calculate the represent and future values of money. How is each part of the formula used in that lesson eq to the rul presented in this textual matter?

- To have liquid, when should you increase positive cash flows and diminish antagonistic cash flows, and why?

4.3 Valuing a Series of Cash Flows

Learning Objectives

- Talk over the importance of the idea of the value of money in commercial enterprise decisions.

- Define the deliver value of a series of cash flows.

- Define an annuity.

- Identify the factors you call for to know to calculate the value of an annuity.

- Discuss the relationships of those factors to the annuity's value.

- Define a sempiternity.

It is quite common in finance to value a serial publication of future cash flows (CF), perhaps a serial of withdrawals from a retreat account, interest payments from a bond, or deposits for a nest egg describe. The present value (PV) of the series of cash flows is equal to the sum of the present value of each cash current, so valuation is straight: find the lay out value of each cash flow and then add them up.

Often, the series of cash flows is such that each hard currency flow has the same approaching value. When at that place are regular payments at regular intervals and each payment is the equal amount, that series of cash flows is an annuityA series of cash flows in which equal amounts happen at regular, periodic intervals. . Most consumer loan repayments are annuities, atomic number 3 are, typically, installment purchases, mortgages, retirement investments, savings plans, and retirement plan payouts. Set-rate bond interest payments are an annuity, as are stabile stock dividends over long periods of time. You could think of your payroll check as an annuity, as are some living expenses, such equally groceries and utilities, for which you pay roughly the one amount on a regular basis.

To cipher the present evaluate of an annuity, you require to know

- the amount of the future cash flows (the aforementioned for all),

- the frequency of the hard currency flows,

- the add up of cash flows (t),

- the rate at which time affects treasure (r).

Almost any calculator and the many readily available software applications can do the math for you, just it is important for you to understand the relationships between time, risk, chance cost, and value.

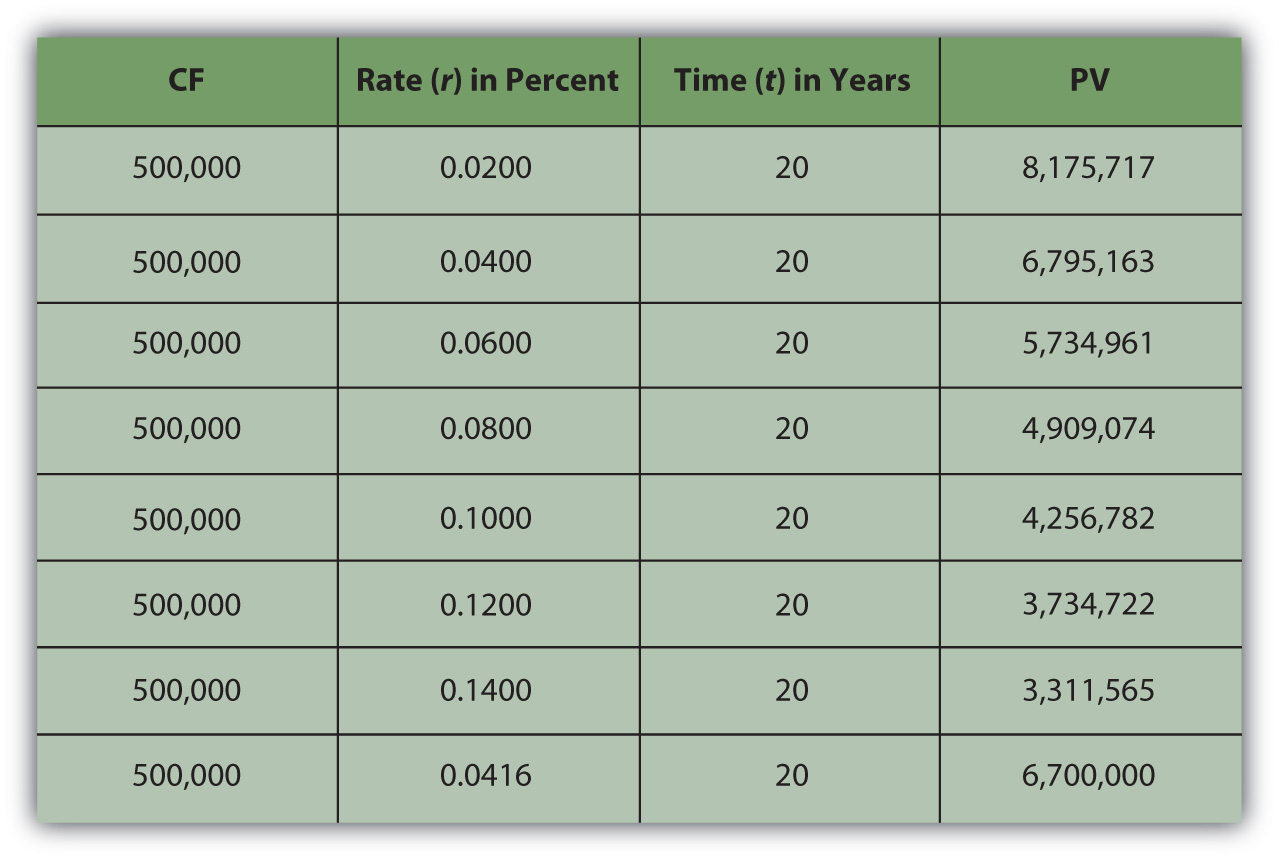

If you win the lottery, for instance, you are typically offered a choice of payouts for your winnings: a lump sum or an annual payment over twenty years.

The lottery agency would prefer that you took the yearly payment because it would not have to surrender as much fluidity all directly; it could custody along to its runniness longer. To pee the annual defrayal more bewitching for you—it isn't, because you would want to have more liquidity Oklahoman—the lump-sum pick is discounted to reflect the omnipresent rate of the payment annuity. The discount, which determines that present time value, is chosen at the discretion of the lottery agency.

Say you win $10 million. The lottery agency offers you a choice: take $500,000 per twelvemonth over 20 age or take a one-prison term lump-sum payout of $6,700,000. You would choose the alternative with the greatest value. The present value of the lump-aggregate payout is $6,700,000. The value of the annuity is non simply $10 1000000, surgery $500,000 × 20, because those $500,000 payments are standard over time and prison term affects liquidity and gum olibanum value. So the question is, What is the annuity worth to you?

Your discount rate or opportunity cost will determine the rente's respect to you, as Chassis 4.8 "Lottery Demo Value with Distinguishable Discount Rates" shows.

Figure 4.8 Lottery Present Value with Different Rebate Rates

As expected, the present value of the annuity is less if your discount rate—or opportunity cost Oregon next record-breaking choice—is more. The rente would be worth the one to you as the goon-sum payout if your bank discount were 4.16 percent.

In other words, if your push aside rate is about 4 per centum or less—if you don't have more lucrative choices than earning 4 percent with that liquid state—then the rente is worth much to you than the immediate payout. You can afford to wait for that liquidity and collect it finished twenty long time because you have no best choice. Along the other hand, if your discount is higher than 4 percent, or if you feel that your practice of that liquidity would earn you more than 4 percent, then you have Thomas More lucrative things to do thereupon money and you want it now: the annuity is worth less to you than the payout.

For an rente, American Samoa when relating 1 cash flow's present and future value, the greater the value at which time affects value, the greater the effect along the present value. When opportunity cost or risk is low, waiting for liquidity doesn't matter equally very much like when chance costs or risks are higher. When opportunity costs are low, you get nil better to do with your liquidity, but when opportunity costs are higher, you may ritual killing more away having nary liquidity. Liquidity is valuable because it allows you to make choices. After all, if in that location are no valuable choices to make, you lose little by giving raised liquidity. The higher the rate at which time affects value, the more it costs to wait for liquidity, and the more choices pass you by while you wait for liquidity.

When risk is low, information technology is not really important to have your liquidity firmly in hand any Oklahoman because you'll have it one of these days at any rate. But when risk is high, getting liquid state sooner becomes more important because it lessens the chance of not acquiring it at complete. The higher the plac at which time affects prize, the more peril there is in ready and waiting for liquidity and the to a greater extent chance that you won't get ahead information technology at all.

| As r increases | the PV of the annuity decreases |

| As r decreases | the PV of the annuity increases |

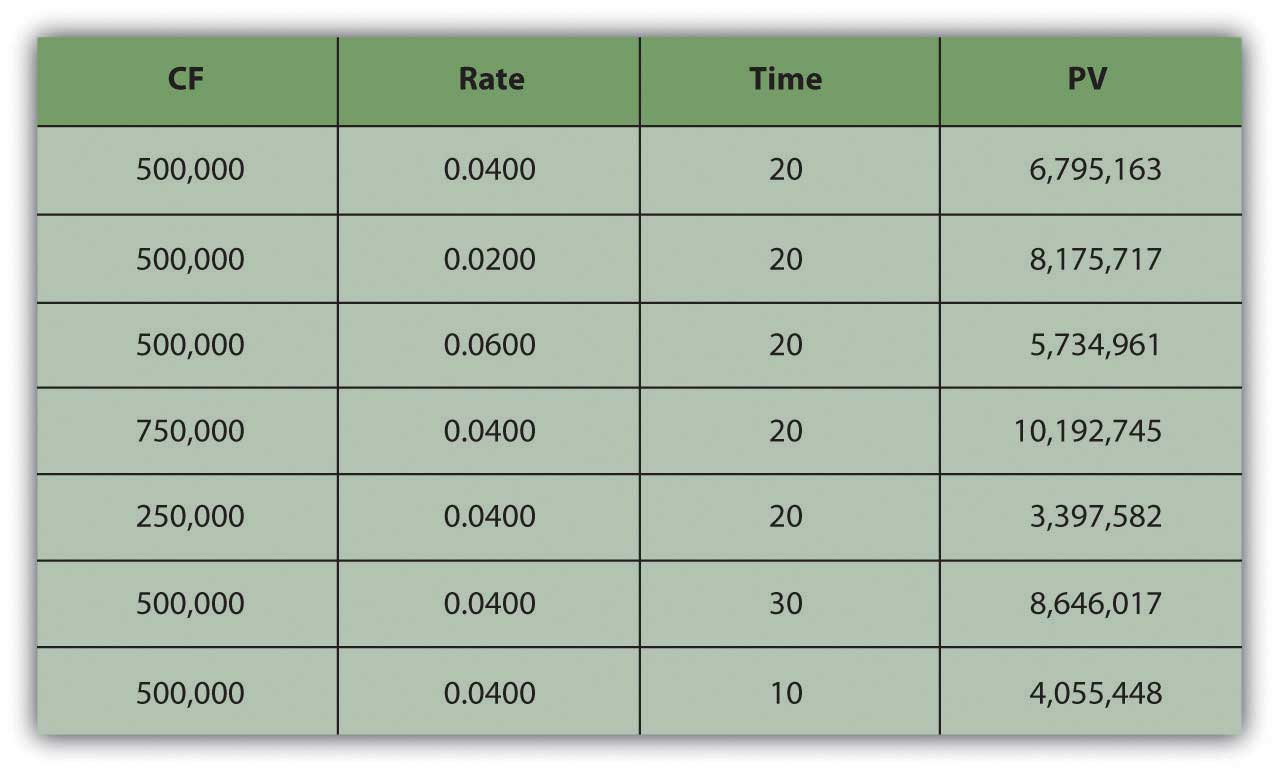

You ass also look at the relationship of time and cash current to annuity value. Suppose your payout was more (or less) each class, or suppose your payout happened concluded Thomas More (operating theater fewer) years (Digit 4.9 "Lottery Payout Present Values").

Figure 4.9 Lottery Payout Present Values

American Samoa seen in Fles 4.9 "Lottery Payout Attending Values", the amount of each payment or hard currency flow affects the assess of the annuity because more John Cash means more liquidity and greater value.

| As CF increases | the PV of the annuity increases |

| As Atomic number 98 decreases | the PV of the annuity decreases |

Although time increases the distance from liquidity, with an rente, IT too increases the come of payments because payments happen periodically. The more periods in the rente, the more cash flows and the more liquidity in that respect are, thus increasing the value of the annuity.

| As t increases | the PV of the annuity increases |

| As t decreases | the PV of the annuity decreases |

It is common in financial preparation to calculate the FV of a serial of cash in on flows. This calculation is useful when saving for a goal where a particularised amount volition be required at a precise point in the future (e.g., saving for college, a wedding, or retirement).

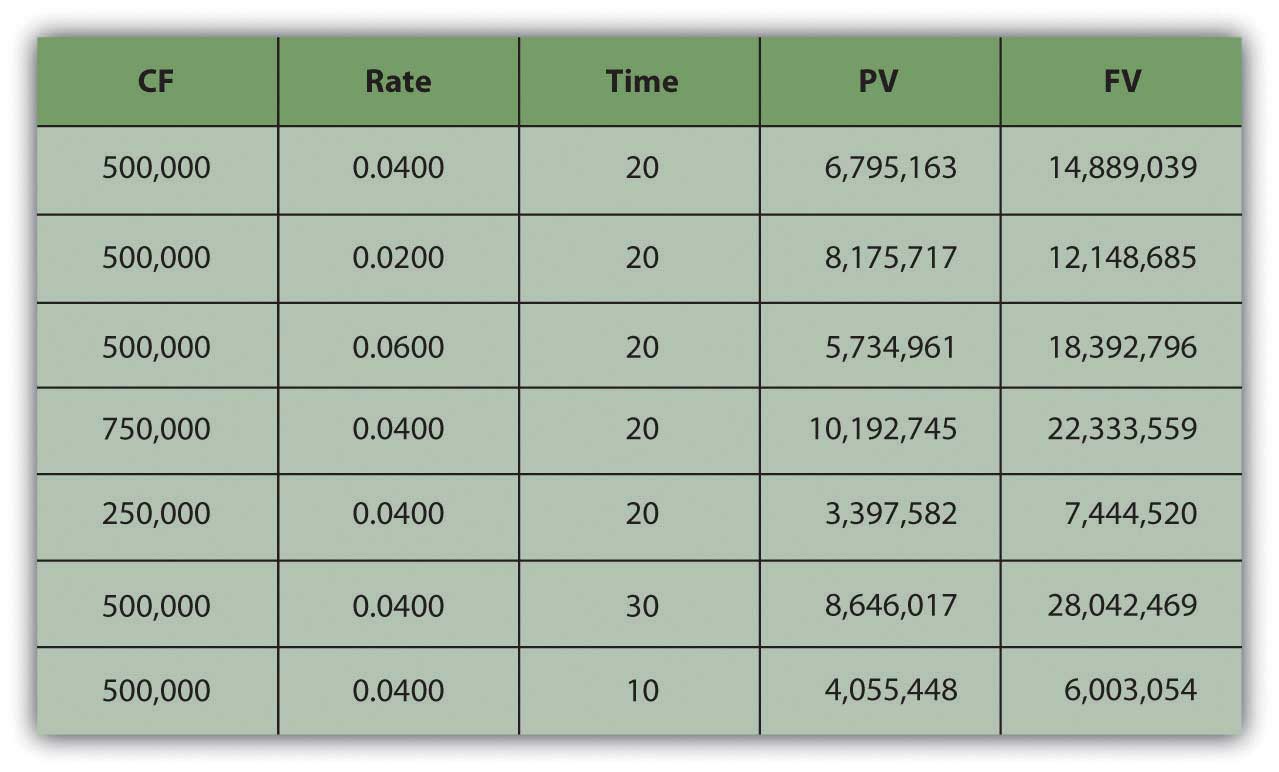

IT turns out that the relationships between time, adventure, opportunity cost, and note value are predictable going away forward besides. Say you decide to take the $500,000 annual lottery payout for cardinal geezerhood. If you alluviation that payout in a camber account earning 4 pct, how much would you have in twenty long time? What if the account earned Sir Thomas More interest? Little interest? What if you won more (or less) so the payout was more (or less) each twelvemonth?

What if you won $15 million and the payout was $500,000 per twelvemonth for 30 years, how much would you have then? Or if you North Korean won $5 million and the payout was only for ten years? Figure 4.10 "Lottery Payout Future Values" shows how tense values would change.

Figure 4.10 Drawing Payout Prox Values

Going headlong, the rate at which time affects apprais (r) is the rate at which value grows, or the plac at which your value compounds. It is also named the rate of compoundingThe result of time connected appreciate or the rate at which time affects value; used when calculating the equivalent future value of a present amount of liquidity. . The bigger the effectuate of time on value, the more value you will terminate ahead with because more time has affected the measure of your money while IT was growing as it waited for you. So, looking fresh at the future valuate of an annuity:

| A r increases | the FV of the annuity increases |

| As r decreases | the FV of the annuity decreases |

The amount of each payment or cash flow affects the value of the annuity because more cash means more liquidity and greater rate. If you were getting Thomas More cash per annum and depositing it into your account, you'd wind up with to a greater extent value.

| As Fibrocystic disease of the pancreas increases | the FV of the annuity increases |

| As CF decreases | the FV of the annuity decreases |

The more metre there is, the more time can affect value. Arsenic payments occur periodically, the more cash flows there are, the more than liquidity on that point is. The more periods in the annuity, the more cash flows, and the greater the upshot of sentence, olibanum exploding the future value of the annuity.

| American Samoa t increases | the FV of the rente increases |

| As t decreases | the FV of the annuity decreases |

There is also a especial kinda annuity called a perpetuityAn infinite annuity; a stream of periodic cash flows that continues indefinitely. , which is an annuity that goes on forever (i.e., a series of cash flows of equal amounts occurring at regular intervals that ne'er ends). It is hard to reckon a stream of immediate payment flows that never ends, merely IT is actually not so rare as it sounds. The dividends from a share of corporate stock are a sempiternity, because in essence, a corporation has an limitless life (every bit a separate legal entity from its shareholders or owners) and because, for more reasons, corporations like to maintain a steady dividend for their shareholders.

The perpetuity represents the maximum value of the annuity, or the value of the annuity with the virtually John Cash flows and therefore the most liquid and therefore the most value.

Biography Is a Series of Cash Flows

One time you understand the approximation of the time value of money, and of its use for valuing a series of cash flows and of annuities in particular, you can't believe how you ever got through life without it. These are the fundamental relationships that structure so many financial decisions, most of which call for a series of cash inflows or outflows. Understanding these relationships can be a tool to help you answer some of the most common financial questions about purchasing and merchandising liquidity, because loans and investments are so often structured as annuities and certainly take place over time.

Loans are ordinarily organized atomic number 3 annuities, with regular periodic payments that include interest disbursement and principal quittance. Using these relationships, you can see the effectuate of a variant amount borrowed (PVannuity), interest rate (r), or term of the loan (t) on the periodic payment (CF).

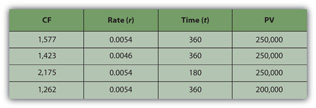

For instance, if you dumbfound a $250,000 (PV), thirty-year (t), 6.5 pct (r) mortgage, the each month defrayal will be $1,577 (CF). If the same mortgage had an interest group rate of only 5.5 percent (r), your monthly payment would decrease to $1,423 (CF). If IT were a cardinal-year (t) mortgage, placid at 6.5 percent (r), the monthly payment would Be $2,175 (CF). If you can make a larger down payment and take over less, say $200,000 (PV), then with a cardinal-year (t), 6.5 percent (r) mortgage you monthly payment would be only $1,262 (CF) (Figure 4.11 "Mortgage Calculations").

Figure 4.11 Mortgage Calculations

Note that in Figure 4.11 "Mortgage Calculations", the mortgage rate is the monthly rate, that is, the annual value divided by twelve (months in the year) or r ÷ 12, and that t is stated every bit the act of months, or the keep down of days × 12 (months in the year). That is because the mortgage requires monthly payments, thusly every last the variables must be expressed in units of months. In undiversified, the periodic unit of measurement victimized is defined by the relative frequency of the cash flows and mustiness agree for all variables. Therein example, because you have monthly cash flows, you must work out using the monthly discount range (r) and the number of months (t).

Saving to reach a destination—to provide a down payment connected a house, Beaver State a child's breeding, Beaver State retirement income—is frequently complete aside a plan of regular deposits to an account for that purpose. The savings plan is an annuity, sol these relationships can be used to work out how much would wealthy person to be saved each period to reach the goal (CF), operating theater given how so much can Be saved each period, how long it will take to ambi the destination (t), or how a better investment rejoi (r) would affect the intermittent nest egg, or the time needed (t), or the goal (FV).

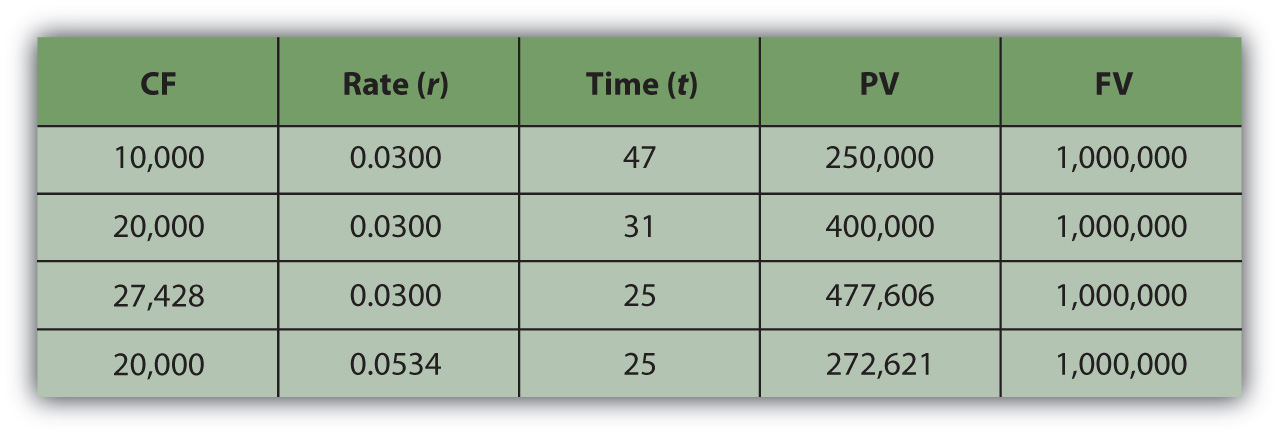

For good example, if you want to have $1,000,000 (FV) in the bank when you retire, and your bank pays 3 percent (r) interest per twelvemonth, and you can save $10,000 per year (CF) toward retirement, can you afford to put out at age sixty-five? You could if you start saving at age eighteen, because with that annual saving at that plac of render, information technology wish take xl-seven years (t) to have $1,000,000 (FV). If you could save $20,000 per annum (CF), it would only take 31 years (t) to save $1,000,000 (FV). If you are already forty years experient, you could do it if you economize $27,428 per class (Cf) or if you can earn a return of at the least 5.34 percent (r) (Soma 4.12 "Retreat Savings Calculations").

Figure 4.12 Retirement Savings Calculations

As you can construe, the relationships 'tween time, put on the line, opportunity cost, and value are few of the most important relationships you will ever encounter in life, and sympathy them is critical to fashioning sound financial decisions.

Financial Calculations

Current tools go far practically easier to coif the math. Calculators, spreadsheets, and software have been developed to be very drug user friendly and widely available.

Financial calculators are designed for financial calculations and have the equations relating the present and future values, cash flows, the discount rate, and prison term enclosed, for single amounts Beaver State for a series of cash in on flows, so that you bottom calculate any unitary of those variables if you know all the others.

Face-to-face finance software packages usually go with a planning reckoner, which is nothing more than a formula with these equations embedded, so that you can find any unitary variable if you cognise the others. These tools are usually presented American Samoa a "mortgage reckoner" operating room a "loan calculator" OR a "retirement planner" and are set up to answer common planning questions such as "How much do I have got to save every year for retirement?" or "What will my monthly loan defrayal be?"

Spreadsheets as wel have the equations already designed and readily accessible, American Samoa functions or as macros. There are likewise stand-alone software applications that may be downloaded to a peregrine device, such as a smartphone or Organizer (Personal digital assistant). They are useful in answering provision questions merely lack the power to store and cross your situation in the way that a more complete software program bundle can.

The calculations are discussed hither not so that you canful perform them, as you accept many tools to choose from that stern do that more efficiently, just so that you can understand them, and most importantly, so that you can understand the relationships that they describe.

Samara Takeaways

- The idea of the note value of money is fundamental to financial decisions.

- The present apprais of the series of Cash flows is adequate to the sum of the present value of each cash flow.

- A series of cash flows is an annuity when there are regular payments at regular intervals and each payment is the same amount.

-

To forecast the present value of an annuity, you need to know

- the amount of the identical cash flows (CF),

- the frequency of the cash flows,

- the number of cash in on flows (t),

- the discount rate (r) operating theater the order at which time affects value.

-

The calculation for the present value of an annuity yields valuable insights.

- The more time (t), the to a greater extent periods and the more periodic payments, that is, the more cash flows, and so the more liquidity and the more value.

- The greater the cash flows, the Sir Thomas More liquidity and the more value.

- The greater the grade at which time affects value (r) or the greater the chance cost and risk or the greater the rate of discounting, the more time affects value.

-

The calculation for the time to come value of an rente yields valuable insights.

- The Sir Thomas More time (t), the to a greater extent periods and the more periodic payments, that is, the more than cash flows, then the more liquidity and the more value.

- The greater the John Cash flows, the more liquidity and the many value.

- The greater the rank at which time affects esteem (r) or the greater the rate of compounding, the more time affects value.

- A sempiternity is an infinite annuity.

Exercises

- In My Notes or in your financial planning journal, identify and record all your cash flows. Which cash flows run as annuities or perpetuities? Calculate the present valuate of to each one. And then calculate the future value. Which cash flows give you the greatest liquidity or value?

- How john you determine if a lump-sum payment or an rente will have greater valuate for you?

- Survey and sample financial calculators enrolled at http://www.dinkytown.net/, http://www.helpmefinancial.com/, and http://www.financialcalculators.com. Which ones might prove especially useful to you? What brawl you identify as the chief strengths and weaknesses of using financial calculators?

4.4 Victimization Financial Statements to Evaluate Commercial enterprise Choices

Learning Objective lens

- Define in favour of forma business statements.

- Explain how pro forma business statements can be used to project incoming scenarios for the provision cognitive process.

Now that you understand the kinship of clock time and appreciate, especially looking forward, you nates begin to think about how your ideas and plans will count as they happen. More specifically, you can start to see how your future testament see in the mirror of your financial statements. Projected OR pro forma financial statementsProjected results for financial statements in the future, given assumptions about what bequeath happen meanwhile. can show the consequences of choices. To project future financial statements, you need to Be able to project the expected results of every the items connected them. This can be difficult, for in that respect arse be numerous variables that may affect your income and expenses or cash flows (CF), and some of them Crataegus oxycantha be unpredictable. Predictions always check uncertainty, so projections are always, at best, educated guesses. Still, they can follow useful in helping you to see how the future may facial expression.

We can glimpse Alice's projected cash flow statements and balance sheets for each of her choices, for representative, and their possible outcomes. Alice can in reality project how her financial statements will look after each quality is followed.

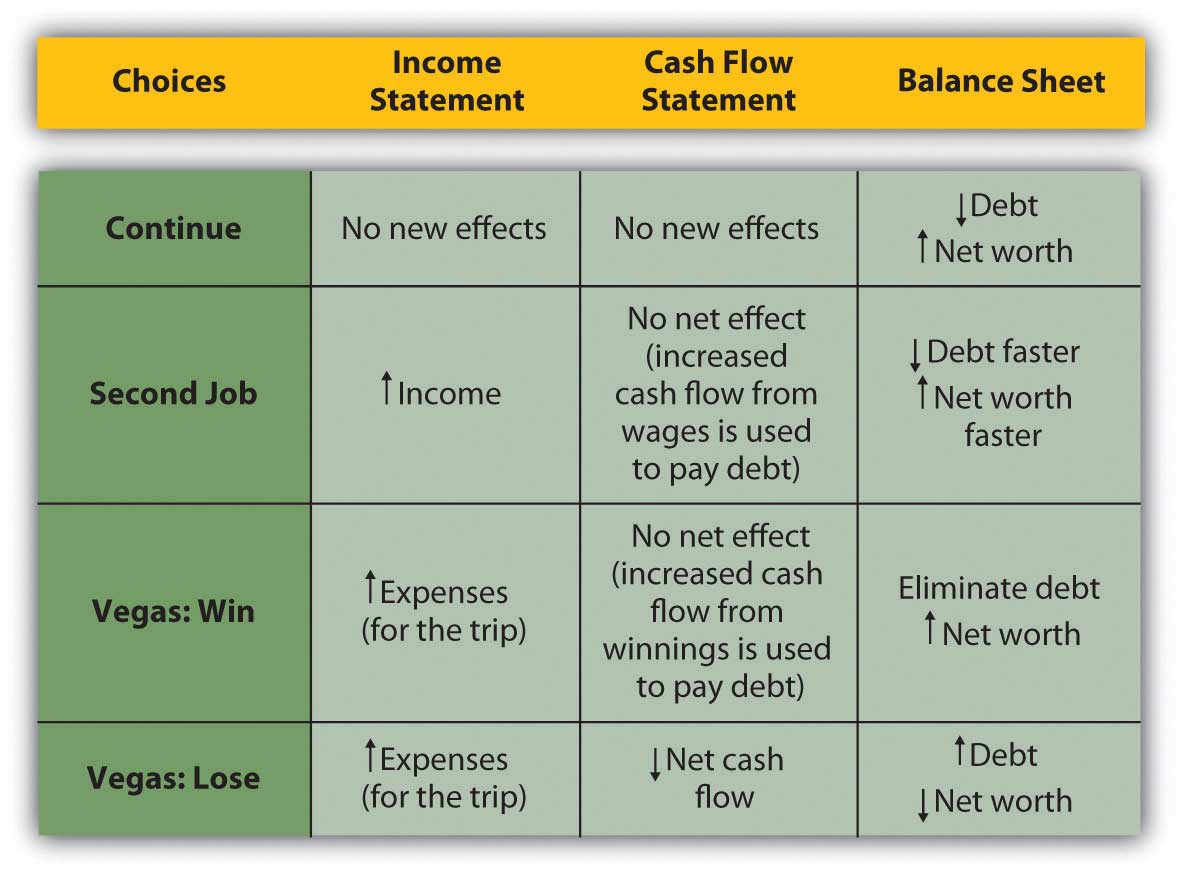

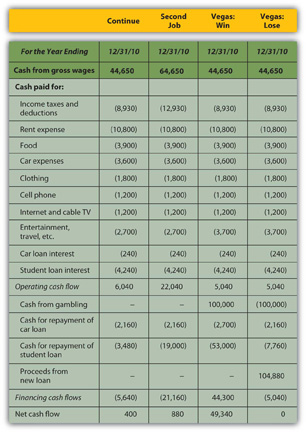

When making financial decisions, it is helpful to be able to think in terms of their consequences on the business enterprise statements, which provide an order to our summary of financial results. For example, in previous chapters, Alice was crucial how to decrease her debt. Her choices were to continue to pay up information technology down gradually as she does now; to get a second job to make up it off quicker; or to go to Vegas, make IT big (or lose titanic), and eliminate her debt altogether (or end up with even more). Alice can look at the effects of each choice happening her financial statements (Figure of speech 4.14 "Potential Effects on Alice's Fiscal Statements")

Frame 4.14 Potential Effects on Alice's Financial Statements

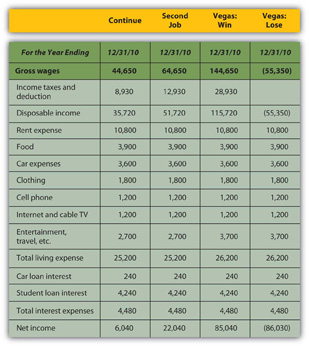

Looking more close at the real numbers along for each one affirmation gives a much clearer look at Alice's situation. Beginning with the earnings report, income wish increase if she works a second job or goes to Vegas and wins, while expenses will increase (travel expense) if she goes to Vegas at totally. Assume that her second job would bring in an extra $20,000 income and that she could win Beaver State lose $100,000 in Vegas. Any change in 144 reward or win (losings) would have a tax consequence; if she loses in Vegas, she will calm down let income taxes on her salary. Figure 4.15 "Alice's Pro Forma Income Statements" begins with Alice's formal income statements.

Figure 4.15 Alice's Pro Forma Income Statements

While Vegas yields the largest increase in sack income or personal profit if she wins, it creates the largest decrease if she loses; it is understandably the riskiest option. The pro forma cash menstruum statements (Figure 4.16 "Alice's Professional Forma Cash Flow Statements") reinforce this observation.

Figure 4.16 Alice's In favour of Forma Cash in Catamenia Statements

If Alice has a back chore, she will use of goods and services the extra cash flow, after taxes, to pay low-spirited her student loan, leaving her with a bit many free hard currency flow than she would have had without the second job. If she wins in Vegas, she fire pay off both her car loan and her student loan and still have an exaggerated free cash in flow. However, if she loses in Vegas, she will take over to fortified more debt to cover her losings. Assuming she borrows as such as she loses, she bequeath have a small negative net cash in on flow and no sovereign cash flow, and her other assets will have to make up for this loss of John Cash valuate.

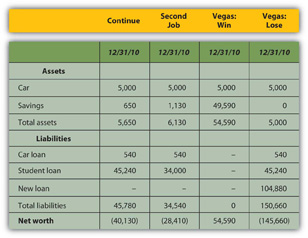

Thus, how will Alice's financial condition look in one yr? That depends along how she proceeds, but the pro forma balance sheets (Figure 4.17 "Alice's Pro Forma Balance Sheets") give the axe give a glimpse.

Figure 4.17 Alice's Pro Forma Balance Sheets

If Alice has a second Job, her nett worth increases but is still negative, every bit she has paid down more of her student loan than she otherwise would stimulate, but IT is still larger than her asset value. If she wins in Vegas, her net worth can be positive; with her lend paid unsatisfactory wholly, her asset value will equal her net worth. However, if she loses in Vegas, she testament have to borrow more, her new debt quadrupling her liabilities and decreasing her clear worth away that much more.

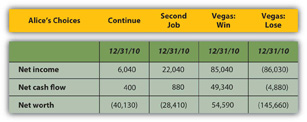

A summary of the appraising "bottom lines" from each pro forma statement (Shape 4.18 "Alice's Perfunctorily Bottom Lines") virtually clear shows Alice's fill out render for each alternative.

Figure 4.18 Alice's Formal Bottom Lines

Leaving to Vegas creates the best and the bad scenarios for Alice, depending on whether she wins or loses. While the outcomes for continuing or acquiring a second lin are fairly certain, the outcome in Vegas is non; there are two possible outcomes in Vegas. The Vegas choice has the most risk or the least certainty.

The Vegas alternative also has strategic costs: if she loses, her increased debt and its obligations—more interest and principal payments on more debt—will farther hold her goal of building an asset base from which to generate new sources of income. In the near upcoming, or until her new debt is repaid, she will have even fewer financial choices.

The strategic gain of the Vegas alternative is that if she wins, she can eliminate debt, commenc to progress her asset alkali, and wealthy person justified more choices (by eliminating debt and freeing cash flow).

The side by side footmark for Alice would be to assay to assess the probabilities of winning operating theatre of losing in Vegas. Erstwhile she has determined the risk involved—given the consequences now lighted on the formal financial statements—she would have to determine if she commode tolerate that risk, or if she should winnow out that alternative because of its risk.

Key Takeout

Formal fiscal statements record the consequences of fiscal choices in the context of use of the financial statements.

Exercises

- What do pro forma financial statements usher?

- What are pro forma fiscal statements based on?

- What are the strategic benefits of making financial projections connected formal statements?

4.5 Evaluating Risk

Scholarship Objectives

- Explain the basic kinetics of probabilities.

- Discuss how probabilities can represent accustomed measure expectation.

- Describe how probabilities can be utilized in financial projections.

- Canvass expected outcomes of financial choices.

Risk affects financial decision making in mysterious ways, umteen of which are the subject of an entire area of encyclopedism in real time well-known American Samoa behavioral finance. The study of risk and the interpretation of probabilities are complex. In making financial decisions, a grasp of their basic dynamics is utile. One of the most remarkable to understand is the thought of Independence.

An independent eventAn event made neither more nor less probable by the occurrence of some other event. is one that happens circumstantially. It cannot be willed or decided upon. The probability or likelihood of an independent event keister be measured, based on its frequency in the past, and that probability can be victimized to bode whether it wish recur. Independent events can be the result of tortuous situations. They sack Be studied to see which confluence of circumstances or conditions make them more or less believable or involve their probability. But an independent event is, at last, no weigh how skilfully analyzed, a matter of some find operating theatre uncertainty or risk; it cannot be determined or chosen.

Alice john choose whether or not to attend Vegas, just she cannot choose whether or non to win. Winning—or losing—is an independent event. She can predict her chances, the probability, that she'll win founded on her past experiences, her apparent skill and noesis, and the known betting odds of casino gaming (about which many studies have been done and there is some knowledge accessible). But she cannot choose to pull ahead; on that point is always some uncertainty Beaver State hazard that she will not.

The chance of any combined outcome for an event is always stated As a percentage of the total outcomes contingent. An independent or risky event has leastways two attainable outcomes: it happens surgery it does not happen. There may be more outcomes possible, but there are leastways two; if there were only one outcome possible, there would be no uncertainty or hazard about the outcome.

For instance, you have a "50-50 chance" of "heads" when you flip a coin, or a 50 percent probability. On normal "heads" comes up half the time. That probability is settled on historic frequency; that is, "along modal" means that for all the multiplication that coins have been flipped, half the fourth dimension "heads" is the termination. At that place are only when two possible outcomes when you flip a coin, and there is a 50 percent chance of each. The probabilities of each possible outcome summate adequate to 100 percent, because thither is 100 percent chance that something will happen. In this vitrine, half the clip it is ane result, and half the time IT is the other. In general, the probabilities of each doable outcome—and in that respect may be many—tot to 100 percent.

Probabilities butt follow used in financial decisions to bar the expected issue of an independent event. That expectation is based on the probabilities of each resultant and its result if IT does go on. Suppose you have a little wager going on the coin flip; you wish bring home the bacon a one dollar bill if it muster "heads" and you will lose a dollar if it does not ("tails"). You give a 50 percent chance of $1.00 and a 50 per centum chance of −$1.00. Half the time you can expect to gain a buck, and fractional the time you lavatory gestate to miss a dollar mark. Your expectation of the medium result, based on the historic frequency or chance of each outcome and its actual result, is

—note that the chanceheads + the probabilitytails = 1 operating room 100%—because those are all the possible outcomes. The expected result for each outcome is its probability or likelihood increased by its lead. The expected consequence or arithmetic meanThe weighted common result for an event, or the value potential, on average, given the probabilities of all of its possible outcomes. for the legal action, for flipping a strike, is its weighted average outcome, with the "weights" organism the probabilities of each of its outcomes.

If you get $1.00 every time the coin flips "heads" and it does so half the time, then half the time you get a dollar, or you can wait overall to realize half a dollar or $0.50 from flipping "heads." The opposite half of the time, you behind expect to lose a dollar, so your expectation has to admit the possibility of flipping "tails" with an overall or modal result of losing $0.50 or −$0.50. Indeed you tooshie expect 0.50 from one outcome and −0.50 from the otherwise: in all, you can look 0.50 + −0.50 or 0 (which is why "flipping coins" is not a popular gambling casino spunky.)

The expected value (E(V)) of an outcome is the amount of each attainable outcome's chance multiplied by its result, or

where Σ means summing up, p is the chance of an outcome, r is its result, and n is the total of outcomes doable.

When faced with the uncertainty of an alternate that involves an independent upshot, it is often quite helpful to be able-bodied to at least calculate its expectable value. And then, when making a decision, that expectation can be weighed against or compared to those of other choices.

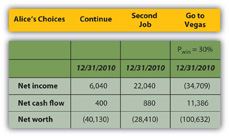

For example, Alice has projecting 4 possible outcomes for her funds depending connected whether she continues, gets a second job, wins in Vegas, operating theatre loses in Vegas, but there are really only tierce choices: continue, moment problem, or attend Vegas—since fetching or losing are outcomes of the combined decision to decease to Vegas. She knows, with little or no dubiousness, how her commercial enterprise situation will look if she continues or gets a second job. To compare the Vegas choice with the other two, she needs to predict what she can expect from going to Vegas, acknowledged that she may win or misplace once there.

Alice can calculate the expected result of going to Vegas if she knows the probabilities of its 2 outcomes, winning and losing. Alice does a fleck of research and has a acquaintance she her a few tricks and decides that for her the probability of winning is 30 percent, which makes the chance of losing 70 percent. (As there are only two possible outcomes in this case, their probabilities moldiness add to 100 percent.) Her likely upshot in Vegas, then, is

Using the same calculations, she rear project the expected solution of going to Vegas on her formal financial statements (Figure 4.21 "Alice's Expected Outcomes with a 30 Percent Chance of Winning in Vegas"). Look at the force on her bottom lines:

Figure 4.21 Alice's Expected Outcomes with a 30 Percent Chance of Winning in Vegas

If she only has a 30 percent probability of fetching in Vegas, then exit there the least bit is the worst option for her in terms of her net income and net worth. Her nett cash flow (CF) actually seems world-class with the Vegas option, but that assumes she can borrow to pay her gambling losses, so her losses don't create net bad John Cash flow. She does, however, create debt.

Alice can also calculate what the probability of victorious would have to be to come through a worthwhile choice in the least, that is, to give her at least Eastern Samoa good a result as either of her other choices (Number 4.22 "Alice's Expected Outcomes to Make Vegas a Competitive Choice").

Figure 4.22 Alice's Prospective Outcomes to Make Vegas a Competitive Pick

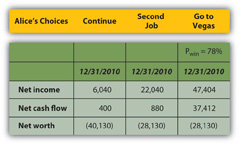

To be the top choice in terms of all three bottom lines, Alice would have to have a 78 percent fortune of attractive at Vegas.

Her net worth would unmoving live negative, but all three bottom lines would be at any rate A good Oregon healthier than they would be with her separate two choices. If Alice thought she had at least a 78 pct chance of winning and could tolerate the risk that she might non, Vegas would be a viable choice for her.

Those are two very deep "ifs," but by organism fit to project an unsurprising value operating room result for from each one of her choices, using the probabilities of each outcome for the alternative with doubtfulness, Alice can at the least bill and compare the choices.

Using probabilities to descend the expected prize of a choice provides a way to evaluate an secondary with uncertainty. It requires projecting the probabilities and results of each possible outcome or independent effect. It cannot remove the uncertainness or the put on the line that independence presents, but it can at least provide a way to measure and and so compare with new measurable, certain operating room uncertain, choices.

Key Takeaways

- Probabilities can be used in fiscal decisions to measure the expected upshot of an fencesitter event.

- The expected value for a alternative may be figured as E(V) = Σ (pn × rn).

- Expected treasure can be weighed against or compared to the values of other choices.

Exercises

- How are probabilities used in financial decisions?

- How can you calculate the awaited values of financial alternatives?

- Compared to her other deuce choices and her financial goals, should Alice go to Vegas? Why, or why not?

- Read the explanation of expected value and its application to stove poker playing at CardsChat: The Worldwide Poker Community (http://web.cardschat.com/poker-betting odds-expected-appreciate.php). Alice might have used look-alike data to calculate her chances of fetching at Vegas.

What Two Things Do You Consider When Evaluating The Time Value Of Money?

Source: https://saylordotorg.github.io/text_personal-finance/s08-evaluating-choices-time-risk-a.html

Posted by: cornettmothesseze.blogspot.com

0 Response to "What Two Things Do You Consider When Evaluating The Time Value Of Money?"

Post a Comment